A week after my ‘Gen X and Gen Y state of retirement‘ post, one of the major credit bureaus (Experian) launched an infographic on the ‘state of credit‘ of each generation.

Your credit worthiness and credit scores are extremely important in today’s economy. They will impact what kind of rate you get on mortgages, student loans, and other forms of credit, potentially costing/saving you tens of thousands of dollars over your lifetime.

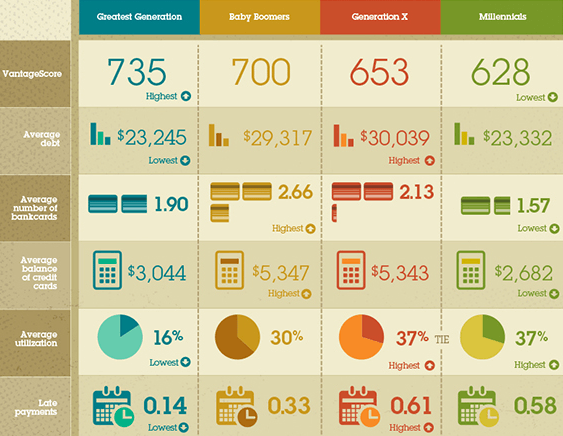

Not surprisingly, Gen X and Gen Y have awful credit compared to the older generations, on average.

How awful?

Well, lets look at this fancy infographic for a second and then dive in to some of the numbers. And I’ll even compare myself to the averages.

How My Credit Stacks Up to the Averages:

I’m officially Gen X, but close enough to Gen Y and have a lot of Gen Y readers here, so we’ll look at both. Before getting in to the credit score results and personal comparisons, versus the average, I thought it would be interesting to first compare my credit usage to the averages.

- Number of Credit Cards: Right now, I have 6 credit cards (just dropped a 7th). This compares to an average number of credit cards of 2.13 (Gen X) and 1.57 (Gen Y). Why do I have so many cards? Doesn’t the almighty Dave Ramsey say that is a bad thing? He does. But I think he’s wrong. I use credit cards for all of my living expenses and have one for each major spending category, which allows me to get an average of about 4% cash back (including 6% cash back on groceries).

- Credit Limit: I have a total credit limit of $75,500 on my credit cards (and that just dropped by $10,000 because I cancelled a newer card I never use). The report did not list this metric, but if you look at the next two metrics, you can calculate it out to be about $14,440 for Gen X and $7,248 for Gen Y.

- Average Monthly Balance: I pay off my balance in full, every single month (versus the Gen X and Gen Y average balances of $5,343 and $2,682, respectively).

- Credit Utilization Ratio: I use about an average of $1,600 per month for a credit utilization ratio of 2.1%. This compares to an average of 37% for both Gen X and Gen Y. Obviously a huge difference.

Credit Score Averages:

Next, I’ll compare my credit score to the averages.

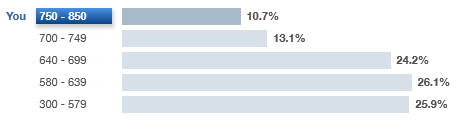

- TransUnion: You can get this score, for free, through Credit Karma. I’m at 769. Anything above 750 is considered “excellent”.

Here’s a chart of TransUnion score averages from a screenshot in my Credit Karma account:

- Vantagescore: Vantagescore is another commonly used credit score that you can get for free through Credit Karma. I check in at 901, considered as “excellent”. The average Gen X’er is at 653 and Gen Y’er is at 628.

Here’s a chart of Vantagescore averages, from a screenshot of my Credit Karma account:

How are Credit Scores Calculated:

How are Credit Scores Calculated:

Each bureau has its own way of calculating credit scores. Here’s a recap of how TransUnion, Equifax, and Experian does it for VantageScore. VantageScore factors the following into your score:

- Payment History: Have you consistently paid your accounts in a timely manner?

- Utilization: How much of the total credit available to you are currently using?

- Balances: What is the total of your current and delinquent account balances?

- Depth of Credit: How long is your credit history and is there a varied mix of credit types?

- Recent Credit: How many recently opened credit accounts and credit inquiries do you have?

- Available Credit: What is the total amount of credit that you currently have access to?

How to Improve your Credit Score

What can we learn from this and some of the metrics you saw earlier?

- Payment history: I never have had a late payment. Important, as it makes up 28% of your score.

- Credit utilization rate is SIGNIFICANTLY lower than the average, which is a good thing – especially since it makes up 23% of the score.

- Balances: paid in full every month and not delinquent. Can’t do better than that.

- Depth of Credit: no current auto loans or student loans. Just credit cards and a mortgage history. I’m potentially getting punished a bit for not having much debt.

- Recent Credit: here’s one spot that you would think I might be getting punished. I have six credit cards, and half of them were opened within the last 16 months. However, as I noted previously, opening new credit cards and closing old ones hasn’t negatively impacted my credit score. This could be due to the higher available credit limit which has reduced my utilization ratio.

- Available credit: another area that I far exceed the average.

I’m not going to even begin to pretend that I have all the answers on how to improve your credit score, but my strategy of using a good number of cards that are paid in full each month, kept open, and with a low credit utilization ratio has seemed to have worked out pretty well.

Credit Score Discussion:

- How do you stack up to these credit score averages and metrics?

- What do you attribute your credit success/failure to?

- Where do you monitor your credit?

Related Posts:

I realize that Dave Ramsey has worked wonders for many people, but I tend to agree more with your methodology of credit card utilization. Have a few cards that you pay off every month, and leverage them to get the best possible cash back/rewards. I myself do still carry credit card debt, which I’m in the process of paying down, but once that is done I don’t have any intentions of closing down any of these accounts. Firstly, it would only hurt my credit rating, and secondly, each of these cards has their own individual rewards/bonuses and advantages. So long as I stay true to my spending budgets and never carry a balance, it’s certainly in my best interest to utilize these bonuses.

This is one of those “only do it if you know why I tell you not to do it” situations. In general, the folks Dave reaches are in 5 figures of CC debt, very house poor, have $50k in car loans and 6 figures of student loans.

Dave tries to beat the “credit cards are free money” thoughts out by going extreme in the opposite direction. However, now understanding why he is going to such an extreme, it’s easier to spot the exception. If you can handle the card responsibly and not carry a balance, then it makes sense to leverage the rewards. Otherwise it’s just a temptation for the people who just spent years digging out from the consequences of their previous temptations.

Well put.

I use Credit Karma as well to monitor my credit.

TransUnion: 780

VantageScore 870. It just dropped from 920 because I just cancelled a Delta Skymiles Card that helped me go on a family trip.

Number of Cards: 2

Credit Limit: $13.5k

Credit Utilization: 1%-5%

Only debt I carry, and plan to only ever carry, is on the house. Student loaned my way through school, but promised myself I would pay it off in the same amount of time that I spent in school. I accomplished that this past year. Went to school for 4.5 and paid them off in 4.

Nice work on the Student Loan Pay off!!! That is the way to do it. Don’t let 4 years of college burden your life with 30 years of loans.

Great scores and good job on attacking debt!

I am Gen Y.

My CK score is 757. I have 2 credit cards and 1 charge card. My utilization is less than 1% because, although I run around $700 through each month, I often pay before the statement cuts. My CC Limit is $22,700 (which obviously doesn’t include my charge card).

I pay my cards in full each month.

I have loans of about $8500.

Hi after reading several of your posts, I’ve gained a lot of knowledge that sometimes makes me look and feel smart around my peers.

I’m 30 years of age and became a legal resident about a year ago which give me the privilege of having a SS# . I’ve always wanted to build a solid credit history but the birth of my SS# doesn’t allow me to at the moment. My credit score fell from 757 to 577 and went back to 746 after a three months(based on the info provided by credit karma).

I think the reason is because my spouse added me to a credit with a limit of $2500 and about 10% utilization also about 8 solid years of great history.

A few months after my 20k student loan was added to my profile/history and caused my score to plunge to 577, so I decided to remove my name off the credit card and my score climbed back up to 746 which I’m assuming is the reason for the increase.

I’m currently a full time student and unemployed, also I have two hard inquiries on my report made before I was added to the credit card.

I’ve had several pre aproved credit card offers in the mail but I’m afraid to sign up because of the lack of history and my employment status.

Can you please advice on do’s and don’t’s to build a solid credit history and a higher score?

Thank you.

I use Credit Kharma, Mint, Manilla. I have a bunch of credit cards. I only carry a balance on the mortgage and pay off my credit cards every month.

Interesting article…one side I would make: You say you pay your balance off in full every month on your credit cards…which is great. However, if you were to run your credit report, it would reflect that you have a monthly balance of $1,648 or whatever your total expenses were for the previous month. The biggest downside I see in current credit score data is that it never really takes into account whether you pay your balance off every month, or whether that value just goes up or down slightly each month. So really, your monthly balance is ~$1000 less than the average Gen Y.

Keep up the great work.

Don’t forget the tried-and-true annualcreditreport.com. Congress has entitled every U.S. Citizen to one free credit report from each of the three major agencies every year, so might as well take advantage! Going this route doesn’t require creating an account and password with yet another third party. The only real “push” you receive is to pay for an official credit score or credit monitoring services.

CreditKarma, etc. pay their bills by advertising credit card offers, so any discerning consumer has to question how impartial they can be. Everything you need to know can be accessed from annualcreditreport.com. As long as you have nothing weird happening and everything is paid on time, low utilization of credit, several years of history, etc. then you’re fine.

The credit score by generation is somewhat surprising to me. I expected with the higher credit utilization among millennials I expected the average credit score to be a little higher. I’m not at all surprised that the “greatest generation” has the lowest average debt and lowest percentage of late payments. Thee is history thee that we can’t compete with. We have never tasted circumstances like what they went through.

Their short credit history hurts their score. Also notice they have the same utilization rate at Gen X with nearly half the average balance, which says they haven’t been extended as much credit.

Overall the numbers are what we would expect: Credit scores are higher with each older generation. There’s not much one can do about having a short credit history, except to keep paying on schedule and allow time to do its work.

I hadn’t considered the length of credit history being a factor in this, which should have been obvious. However length of credit history is a factor that has medium weight toward determining your overall credit score. Credit utilization holds high weight toward determining your overall credit score. I think that is why I was somewhat surprised.

I was pretty surprised to see that I stack up similarly and fall in with the “Greatest Generation”. I’m 26, nearly 27 so I guess I’m Gen Y. I’m happy with this.

Just discovered this website and thus Credit Karma. Awesome tools.

I find CK to run high (almost 60 points at times) for transunion compared to the transunion fico I get with one of my cc accounts. Do you know the origin of the surveyed vantagescore so you know you’re comparing apples to apples?