With last Thursday’s ACA Supreme Court ruling confirming that Congress intended to include subsidies for those on the federal exchange in addition to state exchanges, the ACA has now survived an election, two Supreme Court rulings, and numerous Republican Congressional repeal attempts. Outside of Republicans taking back the White House, maintaining a majority in the House, and grabbing a two-thirds supermajority in the Senate, the ACA is likely here to stay for a while. So, I thought it would be a good time to recap what the ACA is, and then dig in to how it has performed thus far, the winners and losers, and how it can approve.

Most personal finance bloggers avoid the Affordable Care Act (aka “Obamacare” or “Romneycare”, if you will) like the plague, in fear that it might polarize their audience. But I think shying away from such a big topic is a disservice. The ACA impacts all of us – our friends, family, communities, and the nation as a whole. Hopefully by the time you are done reading this, you will agree that I have tried to maintain objectivity and stick to the facts (with a boatload of research and over 2,800 words) versus steering towards the political crap.

As long as the ACA works over the long-term, I don’t care which party takes credit for the idea. Both have a rightful claim: Republicans dreamt it up in conservative think tanks in the 90’s and were the first to implement it (Romney in Massachusetts, which had and still has a nation leading percentage of insured citizens, by a wide margin). Democrats then pushed through the legislation as their platform. Whichever party did not push health reform legislation through as part of their platform was going to work their hardest to discredit the changes and repeal it if it actually had a threat of working and making the other party look good – that’s politics.

Please, no political debates or grandstanding here. Lets stick to what the ACA does, how it works, the impact, winners and losers, and how can it get better – those are the things I want to examine and discuss.

The Affordable Care Act, at its Simplest

The Affordable Care Act, in full, is 906 pages – so summarizing it in one section of a blog post is going to do it a disservice, but I’ll give it a fightin’ effort. What the hell does this behemoth actually do? At its simplest, the ACA’s intent is to increase the number of Americans with health insurance. In order to achieve this, there are three main components:

- Guaranteed issue and community rating: in order to boost coverage for everyone, nobody can be denied coverage because of their age, gender, health risk, pre-existing conditions, lifetime costs, etc. as was commonly practice prior to the law’s enactment. And you are no longer individually rated for premiums – you are bucketed into an age and geography rating.

- The individual mandate: in order to encourage participation, the ACA individual mandate declares that you must have health insurance or you will be have to pay a tax penalty. The goal of this is to get healthy individuals (who may elect to skip health insurance) to join the risk pool and help lower costs for others. A second goal in this is to get low-income individuals insured so they are contributing some cost to their health care (versus getting the services, not paying for them, and leaving the tab with all of us in the form of higher costs).

- Subsidies: in order to encourage participation and help pay for insurance, the ACA offers subsidies for monthly premiums on the health care exchanges for households with income up to 400% of the U.S. poverty line.

The combination of these three components has been metaphorically compared to a 3-legged stool. Without all three legs, the plan (the stool) will completely fail to work.

There are a number of additional components as well that are meant to help keep health care costs in check. Here are a few of the big ones:

- Insurers must have a medical loss ratio (percentage or premiums spent on medical care) of 85% of premium dollars for large group plans (over 50 employees) on medical care (non administrative costs and/or profit make up the remainder) must refund the difference to subscribers, through refund checks or discounted future premiums. The limit is 80% for individual or small group plans.

- All plans must cover an annual preventative visit, 17 preventative services for all adults, and additional preventative services for women, for free.

- The creation of state and federal health insurance exchanges with approved subsidy-eligible plans to ensure minimum coverage and help consumers find and compare plans.

- Raised the age of dependent adult children being able to stay on their parents’ plan from 19 to 26.

How has the Affordable Care Act Performed?

With the background on how it works, how has the ACA actually performed against its goals in its relative 1.5 years infancy?

Number of insured: most importantly, how has the ACA fared in getting more Americans insured? Despite fears that many would lose coverage, there has been a net addition of 15 million newly insured Americans. This has varied pretty dramatically by state. In states that chose to use federal funds to expand Medicaid (mostly blue states), the number of uninsured has been cut in half to 7.5%. States that did not elect to expand Medicaid (mostly red states) have seen a similar percentage of uninsured decline, but are left with a higher percentage of uninsured. The number of uninsured Americans has declined significantly each of the last two years and that will hopefully continue.

Costs: those who were young and healthy, with self-insured (non-employer) plans, saw the disappearance of super high deductible, low premium plans, as they were made illegal by the ACA. If you fall into that group, you’re likely paying higher premiums than you once were.

Everyone else? It is hard to get apples-to-apples comparisons here because premiums can be significantly different from one state or even city to another and hence from one individual to another. For example, Seattle saw ~10% premium rate declines each of the last two years, while Portland will see 6.1% and 16.2% increases. Overall, the ACA marketplace plans saw premiums increase just 2% on average from 2014 to 2015. Employer plans saw a slightly higher change. 2015 to 2016 changes are TBD, but expected to have a slightly higher increase in the 4-5% range (or about ~1% increase after subsidy adjustments). How does this stack up compared to recent averages? Pretty favorably.

As with all insurance, the lowest cost provider frequently changes. It pays to shop around every year.

The economy: so far, the ACA has not turned out to be the job killer that it was predicted to be. The U.S. economy has added over 240,000 jobs per month on average since it went into effect – the largest monthly job gains since the 1990’s, and the unemployment rate has dropped to 5.5%. Certainly, there are other macroeconomic factors at play, but at the very least, the “sky will fall” fears have not played out.

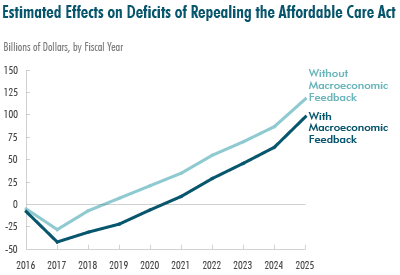

Federal budget impact: this one shocked me a bit, but the non-partisan Congressional Budget Office released a report that determined that the impact of REPEALING the Affordable Care Act would ADD $137 billion to the deficit over the next ten years. It also determined that the number of people with health insurance would drop from 90% of the population to 82% (24 million more uninsured if repealed).

ACA Winners and Losers

In any significant new reform legislation, there are going to be winners and losers. This holds true with the Affordable Care Act. I think it’s important to look at the scale and relative impact of each when considering if legislation has a net plus or minus impact on society.

The ACA winners are as follows:

- More American families: 9.4 million fewer American families are having problems paying medical bills.

- More Americans: of those with a new marketplace plan, 86% were “somewhat” or “very satisfied” with their plan. 11% reported being “worse off” with their new plan, while 5X as many (52%) reported being “better off”. The marketplace plans are superior to the bare-bones plans previously offered in the self-insured marketplace and the increase in costs is more than offset by subsidies. Additionally, most Americans now have significantly more preventative health services and screenings available to them for free. And in total, 15 million more Americans are insured than prior to the law’s enactment.

- Dependents: with carriers now being required to allow dependents to stay on their plan until age 26 (up from 19) there is more leeway for young adults to transition to a working career that offers health insurance coverage.

- Females: due to higher cost of care, otherwise healthy females were charged sometimes more than 50% more on average than males of the same age for the same health insurance. The ACA prohibits gender rating, so this no longer exists. Additionally, a number of female-specific preventative services and birth control are now free for women.

- Anyone with pre-existing conditions: if you were unlucky enough to have pre-existing conditions, you were typically formerly completely denied insurance coverage altogether or charged impossibly high rates. This is no longer allowed. Many of these folks were at risk for medical bankruptcy. They no longer are.

- Anyone who had previously high health care costs: many insurers had lifetime cost caps that if were crossed, you were simply cut off from further expense coverage. Lifetime caps were eliminated with the ACA. Disaster averted for these individuals.

- Some insurance companies: insurance companies that are participating in the new exchanges now have a much bigger pool of insured to draw from which increases their user base and potentially revenue. The ACA opened up completely new markets for some of them.

- Self-employed: those who choose to be self-employed now have a much more likely shot of finding affordable health insurance versus having to take unwanted jobs to rely on employers for insurance.

- Early retirees: similar to self-employed, early retirees will now much more easily be able to find and afford health insurance without needing an employer plan.

- Anyone who has ever had to pay for COBRA: screw COBRA and its ridiculous rates! ACA plans are much more affordable.

- Older individuals: previously, insurers could charge a rate premium to older individuals of 5:1 or greater in 42 states. Now, the premium increase for age has been limited to a maximum of 3:1 of an individual that is 21 years old.

- Low to upper-middle income families: the ACA offers subsidies for monthly premiums on the health care exchanges for households with income up to 400% of the US poverty line, reducing the amount they pay for coverage.

- States that elected to expand Medicaid: have seen significantly fewer uninsured individuals, which has eased health care cost burdens on those states.

And the losers:

- Those with no pre-existing conditions and self-insured plans: in general, if you have been lucky enough to not have any history of pre-existing conditions and you were buying insurance on your own, your rates could be higher than they previously were.

- Young, healthy males with self-insured plans: if you are a young, healthy male with self-insured coverage (non-employer) and are not a part of one of the “winner” groups, you are probably paying more for insurance these days than you were before. The barest of low-cost bare-bones plans were eliminated from the market.

- Healthy high income families: individuals with an income over $200,000 and married filers with income over $250,000 now pay an additional 0.9% medicare tax. Net investment income for those at the same income thresholds is taxed at 3.8%. These new taxes were put in place to pay for the subsidies and Medicaid expansion.

- Some insurance companies: also a winner, many insurance providers are a loser in that their margins could be squeezed by the new medical loss ratio requirement of 80 – 85% of premium revenue being spent on medical care. Also, those insurance companies that offered low value insurance plans have been pushed out of the exchanges completely.

- Employees with “Cadillac” plans: the excise tax to discourage cushy “Cadillac” plans does not officially kick in until 2018, but employees with these high cost plans may see their benefits being scaled back by employers looking to avoid the tax. It has been estimated that the excise tax would impact roughly 16% of plans. Super cushy plans might become only cushy in the future.

- States that elected to not expand Medicaid: states that voluntarily decided to decline federal funds for Medicaid expansion were left with comparatively higher health care cost burden than those that accepted funds.

I know it’s still early, but it appears that so far, there are significantly more winners than losers, and it’s not even close. And even if you fall in to a “loser” category (as I do) at this moment, there is a good chance you will end up in a “winner” category at some point (i.e. when disease strikes, you become self or unemployed, your income drops, or you get to age 50+).

The Early Verdict and How the ACA Can Improve

It is still early, but when you take all of the factual data into account and the number of winners versus losers, it is really hard to argue that the ACA has not been a success. Are there some downsides? Yes. The website sucked in the beginning. Young, healthy males (a niche group that I fall into) are paying more self-insurance. And some very wealthy individuals and families are paying a bit more in taxes. But the data and facts show that there has been a large net plus effect – a large number of Americans have benefited and will continue to benefit from the legislation and millions of lives will be saved both medically and financially. That is a step in the right direction.

Could the ACA be better? While the cost of insurance has tapered and been better than expected, it’s still too damn high compared to other developed nations. The ACA still allows for too much insurance company involvement as middle-men with no true value added. As a result, in the U.S., we spend almost 20% of GDP on health care, compared with about half that in most developed countries. We’re still paying ridiculously high markups for prescription drugs and actual health care expenses because there has never been and still isn’t a true free market in health care – when you need drugs and operations, you need it now – there’s no time to shop around across the country. And the 80-85% medical loss ratio requirements were a good step, but still leave way too much room for abuse by insurers and don’t do enough to control costs.

How do we address all that?

Here’s an idea that nobody raises – why not introduce Medicare/Medicaid as competitive options in the newly formed marketplaces and open them up to everyone, at cost? Steven Brill, did a massive health cost expose that discovered that Medicare has an overall administrative and management cost of about two-thirds of 1% of the amount of the claims it processes, or less than $3.80 per claim. According to a recent SEC filing, Aetna spent $6.9 billion on operating expenses (including claims processing, accounting, sales and executive management) in 2012. That’s about $30 for each of the 229 million claims Aetna processed, and it amounts to about 29% of the $23.7 billion Aetna pays out in claims. Medicare can negotiate prices that are a fraction of what insurers can and their administrative costs are 10% of insurers. On top of that, there is no 20% profit payout to Medicare, and no lavish CEO salaries as there is in the 80% medical loss ratios for insurers. The government is already in the health insurance business, and it turns out they are pretty damn good at it relative to private insurers.

Negotiating power, more than anything else, is what sets medical cost prices. The more negotiating power a provider has, the lower prices will be. Medicare/Medicaid are really good at that – significantly better than private insurers, and would only get better with more participants. If there are insurers that can grow in size/scale/efficiency to compete with the government and/or if users want to stick with a non-government insurance option, then let them. I’m not arguing for a complete government takeover of health insurance, rather, I’d like to see Medicare/Medicaid compete with private insurers, give everyone the choice of coverage, and let the rest work itself out as it may. If the result is government wins and we all go to single payer or insurers win, then so be it. The only thing that SHOULD matter is lower health care costs for every American for now and into the future.

Is this a perfect solution? Nope. Single payer would control costs better, but in this political climate, I just don’t see that as even a remote possibility for a next step. Opening public options on the exchanges is the next step to not just keep costs under control, but actually start significantly trimming them. And shouldn’t that be the ultimate goal?

Update: Trumpcare Fails, ACA Survives, Single-Payer Next?

Related Posts:

Great summary here on what’s transpired over the last 18 months. I think you have your own thoughts which you’re definitely entitled to, but I appreciate all the links and that you’re stating the facts. Although you and I fall within the same bucket of young and healthy males, I have family who has benefit from Obamacare and I understand that something’s gotta give when you’re setting out to help the greater good. It is still mind-boggling how our bordering country has healthcare figured out for the most part and we’re still picking up the pieces. The other aspect which hasn’t been discussed here is that the price we pay doesn’t equate to the quality of healthcare. We may be paying a lot more, but the person signing up for the ACA could and probably is receiving superior healthcare.

This all sounds really complicated. In the UK we have national insurance deductions at source and this tax helps pay for nearly all medical expenses and makes life easier. There are countless people who fall through the NET and having a national insurance policy would make better sense. Complicated!!!

Good article. About my line of work, no less.

The ACA was about expanding access more than cutting costs. We all knew letting people buy insurance after they’re sick will cost a fortune. What other insurance can you buy and file claims with after you need it? Auto? Life? …

Insurers may be “middle-men” of sorts but their job is to control costs, because ultimately people shop for low premiums, and premiums are driven by the core costs. They do this by negotiating provider rates, creating consumer consciousness about use of care, actively managing high dollar cases, looking for fraud and abuse, risk-sharing with hospitals/doctors, and incentivizing wellness. They have a profit motive to control costs less their competitor win the volume.

Single payer would doubtfully control costs better. Volume isn’t everything (see also: Medicare Advantage). Strip away the cost measures noted above (which do contribute to higher admin costs, but lower claims and improve health outcomes)… yea.

It might be a “success” for people but not when you are the middle class. My deductible went up to $6,000 where as before it was $1,000. My copays are now $40 and $70. Not such a success for me. I work for a small company. Small company plus middle class = you are screwed. So I’m glad it’s affordable for some and I guess it would be if you weren’t the one paying for it. What good is insurance if it costs too much to use it? My personal opinion is it’s wealth distribution but Jonathan Gruber already proved that. I don’t see how it can sustain itself and as far as I’m concerned it sucks.

That sounds like it all has to do with your employer and not the ACA. And a $1,000 deductible is unheard of these days – even for government employee plans.

That’s not true. My employer plan (a large corporation) is just over $1000. Plenty of ACA plans on the marketplace with $0 deductible.

Going from a $1k deductible/$40 office to a $6000/$70 ACA bronze plan may or may not have been cost-saving to your employer. (But probably was.) Small group plans are more expensive now under ACA because the groups are not underwritten anymore. Previously, small groups would be underwritten and healthier groups would have better premiums. Now it’s guaranteed-issue.

Also, if the pre-ACA plan did not cover certain services required under ACA, that increased costs to the employer.

It looks like small businesses now get a 50% tax credit on premiums paid as part of the ACA, which would seemingly offset premium increases, even while premium increases have been slowing dramatically: http://www.irs.gov/uac/Small-Business-Health-Care-Tax-Credit-Questions-and-Answers:-Who-Gets-the-Tax-Credit

Here’s a quote from a small business owner when the 35% credit was implemented for the ACA (it’s now 50%): http://www.smallbusinessmajority.org/small-business-profiles/mi/Downtown-Home-and-Garden.php#profile

“The Patient Protection and Affordable Care Act, signed into law a year ago, contains a provision that allows employers to claim a tax credit for up to 35 percent of their insurance premiums in 2010. That means Hodesh, who pays 75 percent of his employees healthcare premiums—$60,000 a year—was able to claim $9,000 on his tax return this year. Knowing that money was coming back gave Hodesh, who had been on the fence about hiring another person, the confidence he needed to make his move.”

Thanks for illustrating my point.

What I’ve noticed about the folks claiming their premiums skyrocketed is that they chanced to land in a small group with unusually low claims or average age, so wound up with well below normal premiums. So when that plan was reconfigured on a typical risk profile, of course premiums jumped. Not because the new rate was unusually high, rather the old rate was exceptionally low. Conversely, those in unlucky groups with high claims got a reduction. Its like someone getting 50% off by lottery that had to start paying full fare. They think they got screwed, but in fact were quite lucky.

And I’m referring to normal health plans that basically had ACA comparable coverage. Not phony “skinny plans” not worth the paper they were written on.

It hasn’t impacted me much one way or the other. I had insurance through my employer (large publicly traded company) before it went into effect, didn’t see my insurance rates/coverage change too much, then switched to another fairly large company that offered insurance to all employers prior to the ACA and have similar insurance as before.

I think allowing Medicare on the marketplace would be a wonderful idea. Odds are, it would prove to be more efficient and effective than private insurance companies and more people would switch to it. If that proves not to be the case, than everyone who says companies can do it better than the government would actually have something to back up their arguments. However, like you alluded to, this would be such a drastic change that I doubt it would ever get through Congress – too many lobbyists and PACs would successfully stop it.

Yes, large groups have pretty much gone untouched under ACA, and most under-65 Americans are covered under large groups. Many large groups are self-funded and do not actually have insurance… it just looks like insurance to you. The employer pays all claims. Otherwise, the large group is insured but premiums are based on their own experience.

It hasn’t impacted me at all: I still have a high-deductible plan through work and my birth control isn’t covered. However, I looked up what my rates would have been if the ACA had been enacted while I was in grad school and they were 3x what I paid for a similar plan. I could have gotten a rate slightly below by going through Medicaid, but 1) I’d still pay the higher cost throughout the year and would have to wait for April to get the subsidy and 2) I would feel bad about using Medicaid’s resources when I’m not poor. The subsidies also would have phased out if I were earning a middle class income, so I think young healthy self-employed middle class women may also be losers under the ACA.

I’m glad you mention some of the positives of Obama Care. So many people are focused on only the negatives, its nice to hear both sides of the issue.

I am not sure I understand the logic on opening up Medicare/Medicaid “at cost” to the general public. Single payer systems are effectively monopolies which obviously gives advantages at the negotiation table; however, my concern would be what do the health systems do to meet the requirements of their operating environment if the government comes in and mandates a price with no competition? What happens to the pay for the doctors? What happens to innovation in the medical community when you only get a double instead of a home run on a blockbuster drug/device? Moreover, many of the costs to process a claim aren’t done by the government… they are done by third party providers (aka insurance companies) who have capacity in their claims processing to deal with medicare/Medicaid claims.

I think you bring up a much bigger issue that really hasn’t been addressed in any meaningful way… how do we balance the costs of providing new/innovative treatments with trying to maintain an affordable healthcare system?

Also, I am not sure you can simply tie the number of uninsured to the premium cost and say “well, clearly the ACA is working”… Much like life insurance, I would venture to guess that a good portion of society is underinsured. Also, the vast majority of individuals who obtain healthcare do not do so on their own… they do it through their employer. Wouldn’t it make sense then that the overall premium increases would be lower with more people heading back to work and being covered by their employer plan which then allows the insurance companies to spread risk more effectively. More people back to work indicate a stronger economy which means the insurance company’s reserves are doing a better job covering losses which leads to a lower premium hike?

I just think readers need to look at these statistics with a grain of salt… the true cost and benefit of the ACA will not be known for a while… but I will give you that if the only goal was to get more people covered by a health plan (regardless of whether it is truly affordable or meets the need of the individual and their family), it succeeded.

I realize some data suggests that monthly premiums have slowed. What concerns me is the (many) news outlets currently reporting how insurance companies are proposing 20%+ increases for 2016 rates. Obviously they need to demonstrate this is needed.

In general, Kaiser Family Foundation is noting that the proposed 2016 increases are larger than 2015. Is this just “pent up demand” righting itself.

It seems it will take more than one or two years of data to suggest that the cost curve is really being impacted by the ACA.

I have contacted my US Senator to encourage him to support legislation that may impact the ACA to help reduce costs or allow more flexible pricing. Unfortunately, the cost of health care hurts retirement and education savings in my house.

Every aspect of rate (increase) development, including all assumptions and projections used, are filed with federal regulators. Any rate increase over 10% (usually by state, or region) gets scrutinized by actuaries that CMS hires to determine whether the increases are sound or not. Some states do their own review of every filing as well.

Frankly, in the early days of ACA nobody knew exactly how things would turn out. How sick the population coming in would be. Some companies (again, by region) underpriced and some overpriced.

Hi Brad, I’d agree, I’m not sure how much the Federal side is looking at it. Typically the State insurance boards must approve insurance increases.

If a company underpriced, they are now asking for 20%+ increases to become profitable again. My concern here would be: are these the same stays & plans that were used in defense of the argument that “the ACA is driving costs down”? Well, the costs aren’t really down, as much as the company just lost millions for a year and plans dramatic increases. Then, we have to ask, “if they had done things right, would costs be down? or is that just a one-year phenomenon?”

For a company that overpriced, they have some limits to how much they can charge.

An insurance company that is losing money in a market asking for a substantial increase is likely going to get something — maybe not every % they ask for, but likely a reasonable bit of it. If the insurance commission does not want to allow the increase and the business is losing money, they will choose to exit the market until the insurance commissioner allows them what they need to at least make a reasonable profit.

It’s just hard for me to accept the “it’s working” argument when we see numerous commissioners being pushed for 20%+ increases. That doesn’t seem like a successful bending of the cost curve. Multiple years of data are likely needed.

Generally good write-up here (as usual).

I come to a different conclusion as to the effectiveness of the ACA as well as the general state of the economy. I would nod to data on the underemployed, wage stagnation, and labor participation rate as an important unspoken counter current to most all the data provided above. But, I appreciate the obvious significant work you have done here and the discussion.

Two important downside you appear to have missed:

1.) The cost of compliance for small to midsize companies is onerous and frustrating. My company, a ~50 million dollar manufacturing company, spends tens of thousands of dollars annually(and it is only increasing)on ACA paperwork and training that would not exist otherwise. This is a boon for CPA’s (like me) or lawyers because it gets more business for us. But, it consumes resources that must be offset somehow. I can’t help but notice the correlation between compliance and insurance cost increases from the ACA contemporaneously with stagnant wage growth. This in spite of an apparent decrease in unemployment which should mean increasing wages normally. I know for certain that our workload and costs increased while our budget did not, this means more people getting paid less to push this paperwork through.

2. Freedom was reduced for thousands (perhaps millions) of Americans. A large number of people were willingly uninsured because they didn’t not like the cost/benefit. It can be argued that they were making a bad choice; but, their choice was a valid one that was voided by the ACA. Hence, only the folks who were unwillingly uninsured while later receiving insurance to their liking as a result of the ACA is a meaningful number. Of course, this number does not exist, but reason stands that a large portion (perhaps a majority) of the uninsured would not be insured if given the choice.

Other important things that we won’t know. Quality of care is intangible and many believe it is dropping. This is a key issue that can’t be quantified easily and cannot be ignored in this discussion.

Finally, there are clearly better solutions out there.

Just to name one, encourage employers (and self employed) to offer something like a HSA (health savings account). Essentially, this could look a 401k plan for health insurance that is coupled with a “high deductible” insurance plan.

I had one for years with a $1,500 deductible (this was high in 2008 when I had it) that my employer paid $1,500 into annually. This meant that I had almost nothing out of pocket besides co-pays which were reasonable.

This plan should allow owner directed investment and should be able to roll over into an IRA when certain funding targets are met. It would encourage financial wellbeing as well as incentivize people to be accountable for their health.

At the end of the day we want better care for less money. The ACA fails because it could do better and it is unclear if healthcare is even any better. Costs are needlessly higher than they should be due to onerous filing and regulatory requirements (this happens whenever you add a 3rd party like the government), and other major costs (malpractice limits, FDA screening costs, etc.) were ignored by the government when the ACA was enacted.

Finally, if the efficient market theory is true in stocks/indexes it should also be true in healthcare (just another commodity). The marketplace has great information availability and is a prime environment for competition between service providers (and those that would enter in a new freer market). Typical arguments about the danger of less regulation are countered by the existence of a legal system (you could sue still) and better access to information by consumers so they avoid bad actors. Alternatively, the ACA reduces competition which increases costs and likely decreases quality provided in the long-term. But, by allowing healthcare to be less regulated you would almost certainly see the cost of care fall off the charts with a corresponding increase in available provider options.

It sounds like you basically would like to go back to the way things were: no mandate, only high deductible plans, no community ratings, tens of millions uninsured because they cannot afford it, or they have had bad luck with their health and are individually a loss for insurers, or they pay more because of their gender. All of that was working splendidly, right? How do you think we got to the point of having more than twice the cost per capita for health care than all other nations, with no let up in cost inflation in sight, and tens of millions left completely vulnerable and/or bankrupt?

You mention freedom, but the thing is we are all stuck with the bill when it comes to healthcare when people cannot afford the bill. Do you think those losses vanish into thin air? No, they are redistributed to all of us. We all pay for it. Mortgage companies require homeowners to have home insurance so they aren’t stuck with a huge loss that can’t be paid – it’s no different. Should we take that away from them, so the prices for mortgages go up for everyone else? Should burglars have the freedom to break into your home and take money from your vault? With the subsidies and expanded medicaid, low and middle income individuals are paying net less than they would have before. That’s a net gain for those individuals, not a loss. And what percentage of high income individuals elected to exercise their “freedom” to choose to avoid health insurance? It’s a strawman argument. Health care is one big ecosystem that we are all a part of, man! Not a picture-perfect, bubbly little snow globe for 1.

And I love high deductible plans – they work great… until you run into health issues. Then what? Oh yeah, pre-existing condition – DENIED!!!